UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

Some investors who don’t follow government inflation reports closely were surprised by CPI staying below 2% in February, but they shouldn’t have been. Firstly, we aren’t headed for hyperinflation or even high inflation above 5%. Secondly, the spike in CPI will come from the stimulus, reopening, and base effects. The stimulus just passed and the base effects don’t start until March. We will have higher CPI next month. The reopening should boost inflation sometime starting this spring or summer.

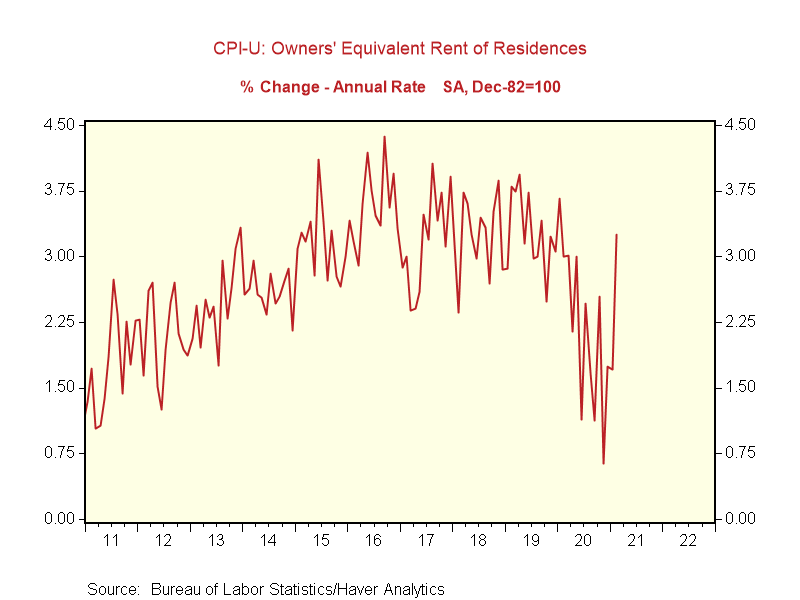

Monthly headline and core CPI were 0.4% and 0.1%. Headline matched estimates and rose 1 tick, while core rose 1 tick, but missed estimates by a tick. As you can see from the chart below, owners’ equivalent rent of residence inflation rose back to where it was in the last expansion.

Once we see overall shelter inflation firm, yearly CPI can rise above 3%. On a yearly basis, headline inflation rose 3 tenths to 1.7% which met estimates. Those who see inflation’s increase as being temporary are mocking those calling for a large rise in inflation. Don’t speak too soon because the rise in inflation hasn’t started yet. Finally, core CPI was 1.3% which was actually down 1 tenth (missed estimates by a tenth as well).

It’s common to hear complaints about groceries costing more while CPI stays low. In this case, the CPI report actually captured higher food costs. Food inflation was 3.6%. Limited service meals and snacks were up 6.3%. That will moderate when spending habits shift away from quick service meals towards dining. On March 19th, indoor dining in NYC will increase to 50% capacity. It has been a very slow process to get back to zero restrictions, but we’re almost there. This is the polar opposite of 12 months ago.

Energy inflation finally went positive for the first time in a year. Energy inflation rose from -3.6% to 2.4%. It will undoubtedly rise to the double digits this spring based on easy comps. As you can see from the chart below, headline PCE inflation can get to above 3.5% if oil rises to $85 within the next few months. Core PCE won’t be affected of course. CPI and core CPI are usually a couple tenths higher higher than PCE and core PCE.

Core commodities inflation finally pulled its weight, but core services inflation was low (compared to recent results). Both were 1.3%. Core commodities inflation is recovering from being near zero for a while. As per usual, apparel inflation was negative (-3.6%) and used cars/trucks had the highest inflation (9.3%). Once the pandemic comps are lapped, used car and truck inflation should go negative especially with increased use of public transportation. It might not have been a long term smart decision to buy a car if the planned ownership was only 1 year, but many people didn’t have a choice if they had to commute to work (buying when demand is high & selling when demand is low).

Within core services inflation, shelter inflation was 1.5%. It will face easier comps next month. It fell from 2.3% to 1.5% in March 2020. It bottomed at 0.1% in May. Medical care services inflation was only 3%. This was one of the few categories that spiked last spring. Finally, transportation inflation was -4.4%.

Massive US Stimulus

The social media posts that say America isn’t doing enough to help people during the pandemic compared to other countries are usually out of context. The full context is America will have done the most to boost the economy and has one of the best vaccination efforts. At the current pace, the US will be 75% vaccinated within 5 months. The U.S. is the 8th most vaccinated country according to Bloomberg. Israel is now fully vaccinated. This has pushed its 7 day average of cases per day down from 8,395 on January 14th to 3,144 on March 10th.

As you can see from the chart above, the expected fiscal stimulus since the end of December is larger than the cumulative fiscal stimulus in the Euro area and Japan up until December as a percentage of GDP. This time the stimulus is going to create inflation because the money will be spent instead of saved. In addition, all the money that was saved in the pandemic will be spent. This will be the biggest growth and inflation boom in a while. America should outperform the rest of the world. America’s impact on global GDP this year is even expected to beat China.

Some investors wonder if this is the new normal. Initially, the Fed stated QE would be temporary. Is fiscal support ever going to go away or will there be a universal basic income? Keep in mind, it’s tougher for Congress to pass a stimulus than it is for the Fed to implement QE. On the other hand, there is political pressure on the Fed to stop QE, while there is political pressure on Congress to keep spending money. Either inflation is not considered to be a tax on the poor or policymakers see no risk of inflation

Sentiment Shift!

The valuation metrics investors focus on depend on sentiment. A stock suddenly becomes cheap when you overlook the PE multiple and instead focus on the price to sales multiple. That’s what happened to software stocks in the past 10 years. On the other hand, investors focused on the price to book value for banks instead of the PE ratio last year. As you can see from the chart below, life insurance valuation metrics shift as well. You want to get ahead of this if you want to avoid getting trampled by the crowd.

Conclusion

The February CPI report was expected to be weak. Its weakness doesn’t mean CPI isn’t a real measurement. We will see it rise in the next few months. The bond market shouldn’t care about this CPI report. It was already priced in months ago. By the time we see 3% CPI prints, the 10 year yield will already be at 2%. The U.S. stimulus is massive compared to other developed countries. If it is a success, other countries might copy America. It will be a fiscal bonanza. Keep in mind, the narrative can deceive you into believing certain stocks are cheap or expensive despite what the objective numbers say or what part of the economic cycle we are in. If the crowd doesn’t like a certain metric, it just moves on to a different one that supports the current valuation/narrative.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.