UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

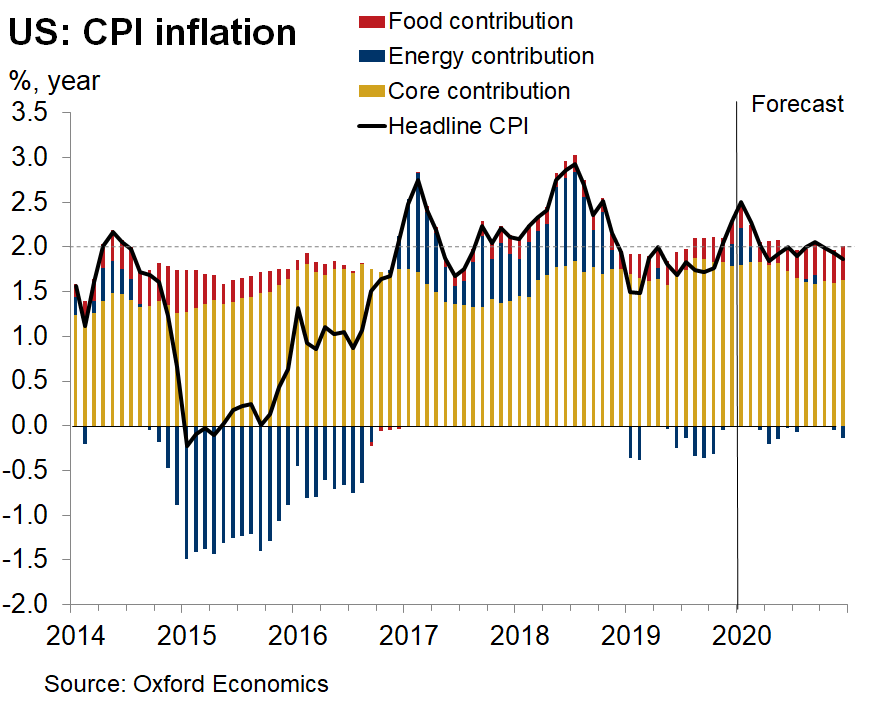

In January, headline CPI jumped and core CPI increased slightly. Specifically, headline CPI was up from 2.3% to 2.5% which beat estimates for 2.4%. Headline inflation was up because of energy. Those who don’t follow this report closely will be surprised by this because oil prices cratered in January due to the effect the coronavirus had on Chinese demand. Energy inflation rose sharply because of its easy comp. Energy inflation increased from 3.4% to 6.2%. Its comp went from -0.3% to -4.8%. Therefore, its 2 year stack actually fell from 3.1% to 1.4%. Energy inflation has another easy comp in February as it is -5%. In the spring, the comp gets harder, but then in the late summer and fall, it gets easy again.

Because real wage growth is deflated by headline inflation, this increase in CPI will suppress it. This decline in real wage growth didn’t hurt consumer sentiment in January as it was near the cycle high. Confidence didn’t wane due to higher energy prices because they actually fell sequentially. They were only strong on a yearly basis. The 2 year growth stack in headline CPI fell because its comp was 44 basis points easier and it only rose 19 basis points to 2.48%.

Yearly core inflation rose slightly, but stayed at 2.3% which beat estimates for 2.2%. Specifically, it rose 2 basis points to 2.27%, but the comp was 6 basis points easier. Core CPI is above the Fed’s 2% target, but the all-important core PCE inflation isn’t. Based on the CPI report, Oxford Economics expects headline PCE inflation to increase 0.2% to 1.8% and core PCE inflation to rise 0.1% to 1.7%. Goldman expects core PCE to rise to 1.75% from 1.6%. Core PCE inflation will stay below the Fed’s target which is why it is biased towards cutting rates.

Medical Care Services Inflation Stays At Cycle High

Energy commodities inflation was 12.1%: fuel oil inflation was 6.5% and gas inflation was 12.8%. Food inflation 1.8% stayed at. As usual, food away from home had higher inflation than food at home because the labor market is tight and food away from home is labor intensive. Specifically, food at home inflation stayed at 0.7% and food away from home inflation stayed at 3.1%.

Core commodities inflation was -0.3%. It was driven lower by used cars and trucks inflation which was -2%. Based on the Black Book used vehicle retention index, used vehicle inflation will increase a bit in the next 3 months. The chart below shows used vehicle retention leads used car inflation by 3 months. New vehicle inflation was low too as it was 0.1%. It’s hard to have pricing power when demand is plateauing.

Medical care commodities inflation was 1.7% which fell from 2.5%. Pharmaceuticals inflation fell from 2.5% to 1.8%. As usual, tobacco and smoking products had high inflation as it was 5.4%. Tobacco firms grow profits by raising prices even though volumes fall in the mid-single digits each year. Its easy to raise prices when your customers are addicted to your product.

Core services inflation rose from 3% to 3.1%. It was pushed higher by medical care services inflation again. Medical care services inflation stayed at 5.1% which is its expansion high. It has been at 5.1% for 3 months. The comp was 0.2% easier, so the 2 year stack fell 0.2%. As you can see from the chart below, hospital services inflation rose to 3.8%. Its monthly inflation was 0.75%. Doctor services inflation was -0.38% monthly. It’s interesting how core CPI is only at 2.3% despite the cycle high in medical care services inflation. That explains why many think it has too low of a weighting.

Shelter inflation increased from 3.2% to 3.3%. It has been above core inflation since September 2012. From July 2015 to today its range has been 3.1% to 3.6%. It hasn’t moved with the national home price index’s growth rate because it is based on rents among other reasons. Lodging away from home had 0.18% monthly inflation which was up from -1.37%. Owners’ equivalent rent inflation was 0.34% monthly and 3.35% yearly (up from 3.27%). Primary rents were up 0.36% monthly and 3.76% yearly (up from 3.69%). Transportation services inflation was low again as it was 0.7%.

Election Risk

The chart below shows the expected movement in the S&P 500 due to the Super Tuesday election on March 3rd (when a slew of Democratic primaries occur) is correlated with Sanders’ odds of winning the nomination.

What this chart doesn’t show is his odds have fallen recently even though he won New Hampshire. He now has a 43% chance of winning which is only 14% above Bloomberg. Bloomberg’s odds are helped by his momentum in the polls and the fact that he is dramatically outspending his opponents. He has spent $114 million on Super Tuesday ads, while Sanders, Klobuchar, Warren, Biden, and Buttigieg have spent $7,071,000 combined.

The hottest topic is whether there will be a brokered convention which is when one candidate doesn’t receive the majority of delegates. Candidates receive delegates in various manners in each statewide race. PredictIt shows there is a 55% chance of a brokered convention. 538 shows “no one” winning the majority of delegates has a 38% chance of occurring (Sanders is at 36%). The working theory is if Sanders wins the plurality, but not the majority of delegates, the DNC won’t choose him to be the nominee as they will want a moderate. While that creates uncertainty, equity investors want to steer clear of Sanders, so it’s a positive outcome.

Conclusion

Higher inflation won’t cause the Fed to hike rates. It is more likely to cut them because core PCE inflation is below 2%. Real wage growth fell, but consumers are still confident. The Democratic primary might have a brokered convention. Equity investors, especially in healthcare insurance stocks, only worry about Bernie winning. The fact that the health insurance ETF (IHF) hit a record high shows you what investors think of his chances of winning (not high). Even if he wins the primary, investors think Trump will win the general election (55% on PredictIt).

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.