UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

The 7.6% decline in stocks pushed the number of cuts expected in 2020 to nearly three. That’s significantly different from recent Fed rhetoric. The Fed recently stated it was fine with current policy and wanted to see how its cuts last year impact the economy before taking any action. The chart below shows the wide chasm between the Fed’s guidance and the Fed funds futures market. As of December, the Fed was expecting rates to go higher within the next couple years.

While the Fed funds futures market doesn’t have a great track record of predicting intermediate term rates, it is accurate in the short term. The Fed will need to express a willingness to cut later in 2020 at its March meeting or markets will revolt. We’ve seen the expectations for cuts increase when stocks fall, but not decline nearly as much when stocks rise. Therefore, if the stock market reverses its losses related to the coronavirus, traders will still expect at least 2 more cuts this year.

The elephant in the room is what the Fed will do once a recession hits. It could be back where it started its hike cycle if it keeps cutting rates during this expansion. The market is pricing in 0.9% rates. If the economy enters into a recession with the Fed funds rate at 0.9%, there is little room for it to cut without going negative. Assuming a recession doesn’t occur this year and the Fed does cut, the closeness to the zero bound will be a hot topic in 2021.

This clearly wasn’t an adjustment to Fed policy. It’s a new cut cycle. The coronavirus helped make sure of this just as the trade war exited the discussion. Even though we’ve seen inklings of an acceleration in growth, weakness related to the coronavirus will likely cover that up. The Fed actually has a better track record of predicting monetary policy than the futures market, but we think guidance in March will be impacted by the futures market. If the Fed doesn’t turn dovish, we will probably see the yield curve invert.

Guidance Ratio Is Falling

2020 was supposed to be the year where earnings recover. That was the implication of the strong rally in 2019. However, because of the coronavirus, EPS growth in Q1 will be below that of Q4. As you can see from the chart below, the average guidance ratio is the weakest since 2015. The time to get long is when guidance and analysts overcorrect to the downside. It’s up to you to determine if we’re there yet, but recognize that many big firms are just starting to understand the impact the virus will have on their earnings.

United Airlines and Mastercard recently put out press releases on how the coronavirus will/has hurt their business. United stated, “As a result of COVID-19, we are currently seeing an approximately 100 percent decline in near-term demand to China and an approximately 75 percent decline in near-term demand on the rest of our trans-Pacific routes.” Mastercard stated “we now expect that if the trends we have seen recently — primarily in our cross-border drivers — continue through the end of the quarter, year-over-year net revenue growth in the first quarter will be approximately 2-3 percentage points lower than discussed on our January 29, 2020 earnings call.” Mastercard and Visa are widely held by growth oriented hedge funds. Let’s see how much courage they have in their convictions as these stocks are hurt by the virus.

Temporary Staffing Demand Falls

Most economic data have been solid outside of the reports where the coronavirus is having an impact. The chart below shows an exception as the 4 week moving average of temporary staffing demand is down yearly. This isn’t a new trend which is why we say it’s not related to the virus. Temp staffing is important because these jobs are the most impacted by demand. If a firm sees weakness in demand, it can more easily let go of temp workers than full-time ones which require mass layoffs. It’s tougher to re-acquire new full-time workers than temp workers.

The monthly BLS labor report shows temporary help services employment has been down yearly for 13 straight months. The only good news is the easier comp helped yearly growth in January rise from -1.4% to -0.5%. There has never been a longer streak of negative yearly growth without the economy either going into a recession or coming out of one, but the data only starts in 1990, so it’s tough to draw conclusions that a recession is about to be here. The modest yearly declines certainly lend support to the possibility that a recession isn’t close. The positive thesis is helped by the lowness of jobless claims.

China Hasn’t Recovered

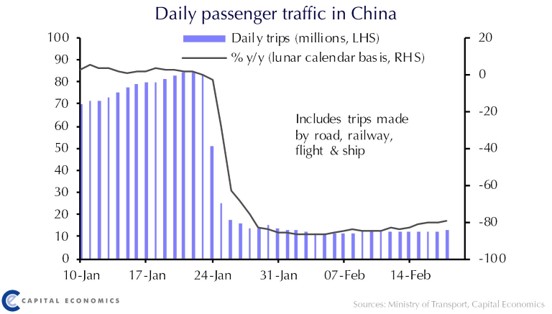

The growth in the number of new coronavirus cases in China has fallen, but economic activity hasn’t come close to fully recovering. Chinese car sales fell 92% in the first 2 weeks of February. As you can see from the chart below, the number of daily trips in passenger cars has fallen about 80% consistently from last year. The number of daily trips hasn’t recovered much.

It’s possible that the decision to quarantine citizens does more harm than good. We will see which approach is best soon enough because we had China do a quarantine, while Italy isn’t about to close its borders even though the number of cases is rising there. The prime minister of Italy stated, reintroducing Schengen borders to prevent the virus from spreading “is a draconian measure that does not meet the needs of Italian citizens in the field of containment of infection.”

Conclusion

The Fed will be pressured into cutting rates further in 2020 even though it previously stated it would wait to see the impact of its 2019 cuts before taking action. The coronavirus is pushing the number of rate cuts expected higher and earnings revisions lower. Mastercard and United Airlines updated investors on how they think the virus will impact their businesses. Temp employment is falling which is a bad sign for the economy. Chinese passenger traffic hasn’t recovered yet even though the growth in new coronavirus cases has slowed.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.