UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

The stock market is very erratic. One day it ignores bad news and the next day it treats it like the end of the world. This can make you think you are crazy. For example, COVID-19 cases and hospitalizations have been rising for a few weeks. The stock market ignored that until it didn’t. It panicked on Wednesday even though we already knew COVID-19 was getting worse for weeks. We have also known for a couple weeks that a stimulus isn’t coming, for now at least.

When stocks were riding high a couple weeks ago it seemed like the market was fine with a stimulus coming in early 2021. Now, it can’t wait. We have known for a couple weeks that Pfizer’s vaccine results would be released in mid to late November. Now, all of a sudden, the market is very scared we have no data. Somehow no data is a bad sign. Two of the phase 3 trials restarted in America last week. Did anyone expect them to tell us anything major by the end of October? The market has decided it has no patience even though policymakers have warned for months that this winter could be bad for COVID-19.

Investors have fear; nothing sounds good to them for now. As you can see from the chart above, 24.1% less small businesses are open now as compared to January. This data point hasn’t moved for weeks. Let’s not pretend the economy is in dramatically different shape now as compared to September. On the other hand, you can argue, the market thinks COVID-19 will make November much worse than October.

Current conditions in the Consumer Confidence index rose from 98.9 to 104.6 and earnings season has gone very well. However, the market has decided any good news doesn’t matter because we are about to go off a cliff next month. It is extending the spike in hospitalizations to infinity and ignoring the possibility a vaccine prevents this winter from being a disaster.

Energy Is This Decade’s Loser

You might say we are being overly dramatic about how the market is reacting because the S&P 500 is only down 7.5% from its October peak and 8.7% from its record. That’s true, but look at the cyclical stocks. Many big cap energy stocks have made new lows. They are doing worse than in March. The market has quickly changed from being optimistic to pessimistic about a recovery. The oil services ETF (OIH) fell 13.2% from its October high and is down 66% year to date.

Energy is historically a very volatile sector, but this is undoubtedly in the record books as one of the worst downturns in history. Because it is worse than any other energy decline, we need to compare this to the worst sector declines in the past 30 years. The chart above shows the drawdown in the tech sector in the early 2000s and the financial sector in the late 2000s after the housing crisis. The current energy weakness is nearly as bad as those two were. You can say this is the once in a decade crash in one of the S&P sectors.

This could be the buying opportunity of the decade like the banks and tech were after their crashes. Remember, prior to the financial crisis, in 2007 and 2008 energy outperformed remarkably. This is its turn to crash. Energy crashed from 2014 to 2016, but that wasn’t enough. It’s back to falling again. Eventually, low prices become the cure for low prices because projects get canceled and scarcity sets the price. The idea that the oil market is suddenly going to be in balance, when the economy reopens, without the 13 million barrels America was once producing is ludicrous. This is a cyclical decline. There isn’t enough green energy to make up for the lost energy, meaning it’s not a secular decline.

Housing Is On Fire

The housing market continues to stay hot. Prices are starting to spike. Such high price growth might limit demand especially if rates rise. Luckily for housing, rates are falling as investors fear an economic slowdown. The August FHFA home price index showed yearly growth rose from 6.5% to 8% as the chart below shows. This type of price growth is unsustainable as it is the highest since March 2006. Peak growth in the 2000s housing bubble was 10.7%. Unless we have a scenario with very easy comps, such growth won’t be repeated.

The MBA applications index also was strong. In the week of October 23rd, the composite index was up 1.7% weekly which followed a 0.6% decline. Refinancing was up 3% weekly after increasing 0.2%. The average 30 year fixed mortgage rate was 2.8% last week which was a record low. Purchase applications were up 0.2% weekly after falling 2%. Yearly growth was 24%. We have seen double digit yearly growth for 23 straight weeks.

Cheap Banks

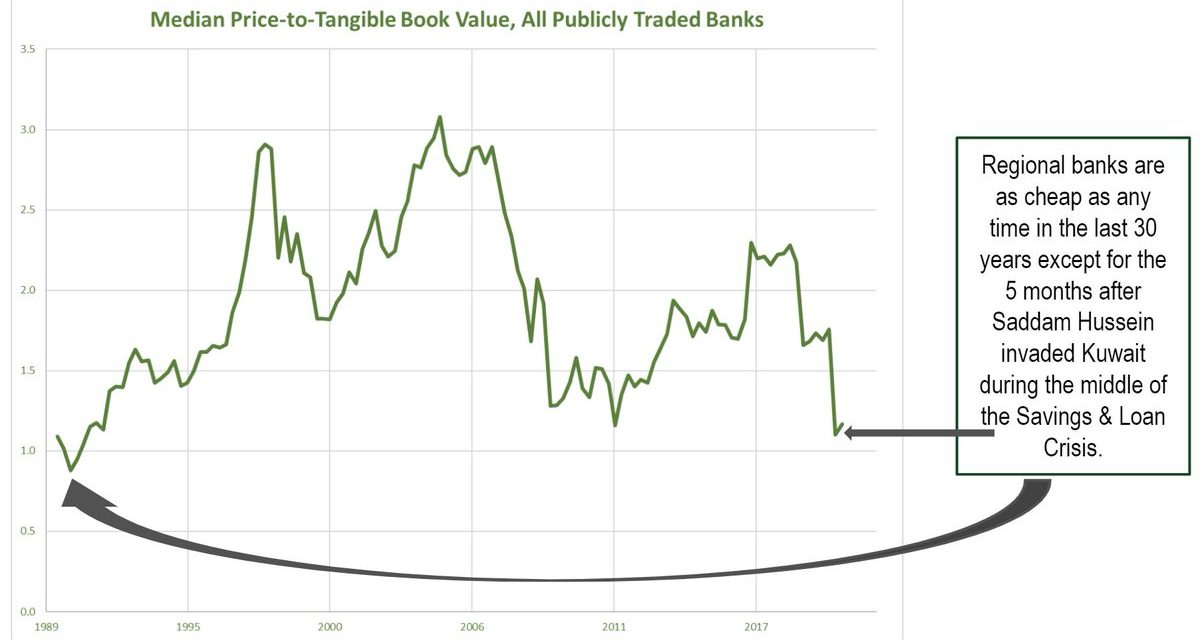

It’s not that hard to see why banks could make a good investment because loan losses are limited, they are well capitalized, mortgage lending is strong, and deposit growth is strong. The banks just need the economy to keep recovering and long yields to rise a bit to help their interest rate spread. Even though the banks aren’t in bad shape like after the financial crisis, they are very cheap. As you can see from the chart below, the median price to tangible book value of all publicly traded banks is lower than the trough after the financial crisis. The banks are the cheapest since the worst part of the savings and loan crisis in the late 1980s.

Conclusion

Investors decided to fear the same things they were ignoring two weeks ago. COVID-19 was spiking in the Midwest and France when the market was near its record. Now it suddenly cares about this negative. Furthermore, the recovery has been gradually slowing for a while. It seemed like 2 weeks ago the market was fine with waiting for a vaccine in November and a stimulus in January, but now it wants help sooner. The energy sector is in one of the worst bear markets any sector has experienced in the past 30 years. It is nearly as bad as the financial sector after the housing bubble and tech after the dot com bust. Banks are the cheapest since the 1989 SNL crisis.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.