UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

Some claimed that when the Fed expanded repo operations, started another round of QE, and cut rates to zero, that it had nothing left to ease financial conditions. That was mistaken analysis. The Fed unveiled new tools to deal with this crisis, which are a massive deal. Firstly, on Friday the Fed stated it would expand its asset purchases to muni bonds which was important because the premium on muni yields over treasuries hit a higher peak than in 2008. Plus, muni bond ETFs were trading below their net asset values. There was some concern with how cities’ budgets would look with the increase in unemployment. The Boston Fed is lending to eligible banks and financial institutions which can use municipal bonds (single state and other tax exempt munis) with maturities of less than 1 year as collateral.

Ordinarily, you’d say the Fed buying munis is a big deal, but we don’t live in ordinary times. March 2020 was an extraordinary month that will go down in financial history as such. The big news on Monday was something we have discussed for a few days on Twitter. The Fed is buying corporate debt like other central banks. In a technical sense they aren’t because they set up special purpose vehicles (SPV) owned by the Treasury. The Treasury puts up some money and the SPV borrows from the Fed. The decision to effectively buy corporate bonds is a big deal because credit spreads have been widening recently. The Fed did an end-around what most thought was illegal to support the economy.

It took about a 30% drop in stocks for the rule book to be thrown out the window. The new rules are that the Fed can’t own more than 20% of any one ETF or 10% of an individual corporate bond. The LQD and VCLT ETFs rallied sharply on this news. They had been trading below their net asset values. It’s seems likely that the Fed won’t be shy about keeping this program up until it is very clear the situation is rectified.

Small Business Gets Help

Finally, the Fed plans to set up a “Main Street Lending Program” where it will funnel money to small businesses interest free for 6 months. The money can be paid back over 4 years. This plan also uses SPVs. We previously did an article saying small business was in dire straits. The situation gets better with free access to capital and a potential fiscal stimulus. We will be watching the March ADP report to see how quickly small firms shed jobs. Obviously, the elephant in the room is how long the economic shutdown lasts. The good news is the number of new daily cases in Italy has been stabilizing. America is a few weeks behind Italy. As the number of daily new cases start to fall in April or May in America, there will be increased discussions to reopen the economy. Wuhan plans to reopen on April 8th.

If small firms are hit the hardest and recover the slowest by/from this recession, it will be the 2nd recession in a row that occurs. As you can see from the chart above, large firms were hit the hardest by the 2001 recession and recovered the slowest. That was a mild recession for all firms outside of tech. The 2007-2009 recession was a disaster for small and medium sized firms as their net job growth didn’t recover the recessionary losses until 8 years after the recession.

Where The Job Losses Will Be

The issue with this economic shutdown is it’s different from the typical recession which hurts a particular area of the economy. In the early 2000s, you had tech and telecom firms get hurt. In the late 2000s, you had homebuilders, real estate, banks, and investment banks get hurt, along with home buyers. The fact that a house is most consumers’ biggest asset made it a big deal. Plus, the banks nearly failed. This current recession could be worse because every area of the economy is impacted and they are impacted hard. The only saving grace is it should be short lived. We don’t know that for sure, but we do know that Wuhan is reopening after about 2.5 months of being closed.

There is a massive swath of the labor market directly or indirectly impacted by this shutdown. The U.S. is a service-based economy. That means a lot of person to person contact. As you can see from the table above, 12% of the labor market is directly affected by COVID-19. On March 21st and March 22nd, OpenTable restaurant bookings were down 100% in America. This type of decline can only occur in a mandated shutdown. 7.3% of the labor market is secondarily impacted by this shutdown. The good news is grocery, health, and online retail are hiring people. However, it’s not enough to counteract the tidal wave of job losses. 12.8% of workers are non-essential and can’t work from home. This all adds up to 32% of the labor force.

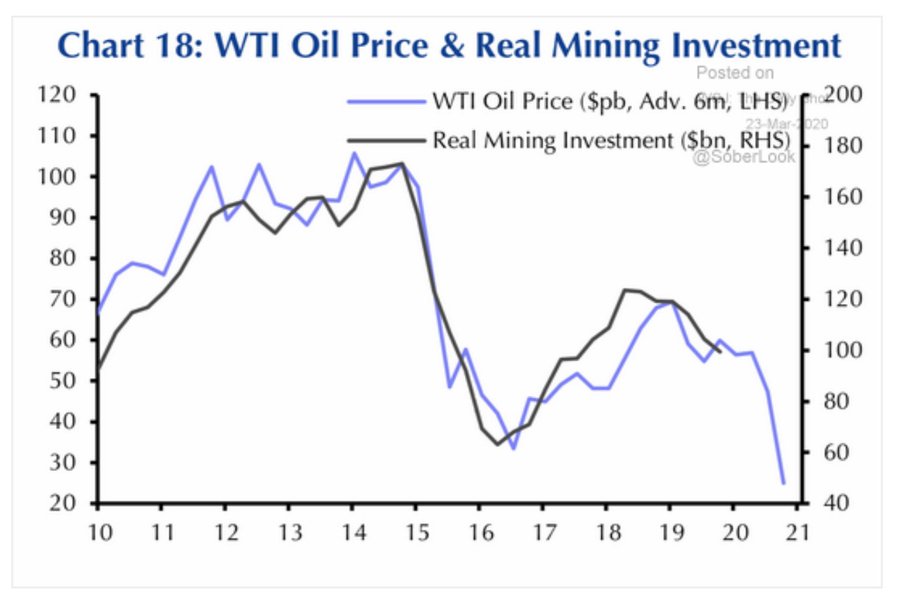

Mining Investment To Be Hurt Badly

The energy industry is in dire shape as even the super major drillers are seeing their stocks collapse. The good news is the oil and gas extraction industry doesn’t employ a lot of people. It only had 157,000 workers in February. Its employment fell about 60,000 after the fracking industry cratered in 2014. The bad news is the decline in oil prices will hurt mining production which will hurt industrial production similar to the 2015-2016 manufacturing recession.

A Rebound In South Korea

The situation on COVID-19 isn’t all dire news. Italy has seen a stabilization in the number of new cases per day. This shouldn’t be a surprise because the country has been on lockdown for a couple weeks. Furthermore, the number of new cases in Lombardy, Italy (hardest hit area) fell from 3,251 to 1,691 to 1,555 (March 21st to the 23rd). One of the earliest hit countries, South Korea has seen a big rebound in exports in the first 20 days of March.

Conclusion

The Fed went all in for real this time by buying muni and commercial bonds. This should help the plumbing of markets and increase investors’ risk appetite in the medium term. Small business and individuals will need all the help they can get from the Fed and the government. That’s not a political statement, by the way. However, the cost is that we could be borrowing from future prosperity to recover from this crisis (something we will examine in future articles). 32% of the labor market will be hit hard by COVID-19. Energy is in serious trouble because of the price war and decline in demand. The good news is the number of new cases in Italy is stabilizing and South Korean exports are rebounding.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.