UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

If you are actively managing your portfolio, you might not even notice the correlation between the overall stock and bond markets. However, you might notice which of your stocks are long and short durations plays. This annoys a lot of fundamental investors because they don’t look at their portfolio through that lens. They try to buy good businesses that will grow their free cash flow and eventually return it to shareholders. That’s a fine ambition, but you might want to alter your portfolio if you find that all your stocks are of one variety.

Even though you’re looking at the fundamentals, you have a new risk if all your stocks are long duration plays. You don’t need to sell because of this. Use this as a clue that some of your stocks might be fully valued. Valuation is certainly part of the lexicon of fundamental investors while macro largely isn’t.

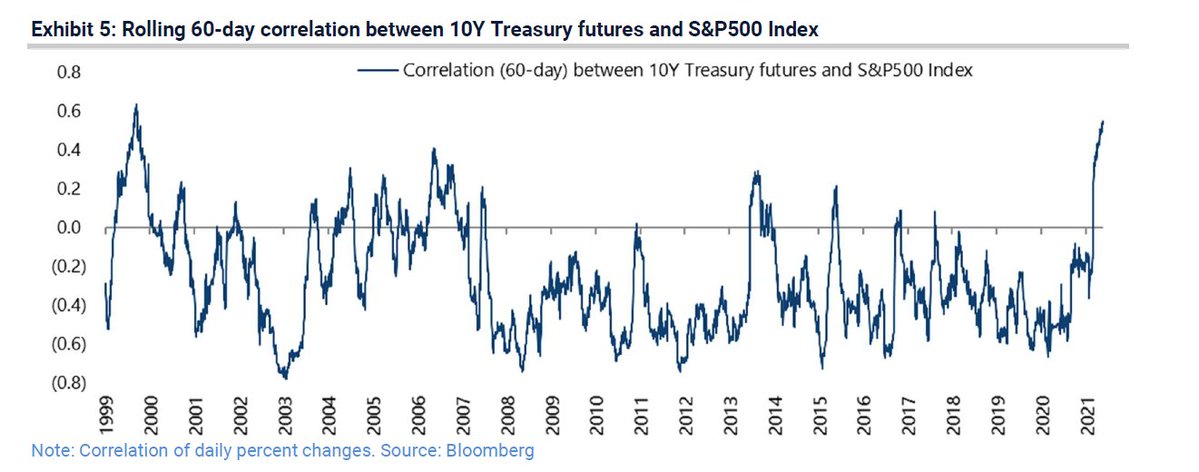

If you are in a passive fund with stock and bond allocations, you probably noticed that in the past couple of months, stocks have been highly correlated with bonds. This is shown in the chart below.

From the outside looking in, this doesn’t sound terrible because the stock market isn’t down much. Why would anyone care if the S&P 500 has fallen 3%? People care because bonds are supposed to be a cushion for equity investors. Investors who have 60% of their portfolio in stocks and 40% in bonds expect to lose less than the S&P 500 when stocks fall. When they don’t lose less, they wonder why they are in bonds. In this case, they are earning less over time and still feel the brunt of day-to-day volatility.

We are sure some people are looking at this chart and wondering why anyone with bonds cares if the correlation has been positive for a couple months. It looks like the positive correlation spikes are only temporary. Passive investors are worried because there is a widespread belief that yields can’t fall much further. Since the 10 year yield is at 1.58%, investors wonder if bonds can continue to rally when stocks fall. If you own bonds, but don’t think they will provide good returns over time, you must alter your portfolio instead of getting frustrated with the results!

This correlation won’t last. The action in the past 2 months is triggering a real fear though. Investors have come up with creative ways to generate returns without bonds. Some replace treasuries with ‘bond like’ dividend stocks. There is no perfect way to solve this problem. Keep in mind, the portfolio with 60% in stocks 40% in bonds wasn’t the perfect solution either even when yields were higher.

Venture Capital Like Returns

The latest trend among retail investors is to try to find stocks that can generate 10x returns. The theory is that these returns are so large that they can make up for losses. There will be losses if you are searching for big wins. It’s a dangerous game because this new mantra throws out some of the basic tenants of value investing. The biggest tenant is taking profits when stocks become expensive. This new investment concept tells investors they shouldn’t sell after their stocks become ‘expensive.’ It ignores the concept that companies don’t all become the next big winner.

There is huge survivorship bias in just studying the biggest winners. No one applauds the investor who takes a 30% profit at nearly the correct time. Old style investors believe they need a margin of safety. They actually sell stocks even when there might be more room for them to rise. Many value investors believe they shouldn’t sell at the exact top. They prefer to sell early because it shows they were prudent. In the long run prudence wins. It’s easier to stay prudent than it is to predict the few stocks that will become the next big winners.

At the same time, it’s also wise to incorporate some of the lessons these new ‘hold forever’ investors teach. You can learn from everyone, especially investors who have done very well. The best takeaway from the new mantra is to avoid selling a great stock because of negative headlines. Don’t be so easily swayed by noise.

With these concepts in mind, let’s review the data in the chart above. As you can see, venture capitalists rarely pick the huge winners you hear about non-stop. Under 4% of dollars invested go to businesses that multiply by at least 10X. Venture capital investing is riskier than investing in public companies since many startups don’t have sales. There are also bigger rewards with VC investing. Therefore, you can argue your odds of getting a 10x stock are even lower than 4%. There is a possibility that all these risky stocks retail investors love go to zero.

Furthermore, it’s possible that there will be fewer big winners in the tech sector the next decade that there were in the prior decade. Everything is cyclical. If you are looking for amazing returns in the exact same fashion as the masses, then it’s not going to work out. You need to look in new places. Furthermore, the very act of looking for a huge winner is too popular. Now might be the time to play it conservative. If you can find a safe consumer staples stock that can return 10% per year with low volatility, take that. You won’t regret such a decision. There is always time to find huge winners. Don’t be impatient. If you take a big hit, the game is essentially over. Staying in the game is extremely valuable. Don’t take in for granted.

Conclusion

Lately stocks and bonds have been correlated. If you are worried bonds won’t save you from volatility, then change up your allocation. Don’t be like a deer in headlights. Some investors are looking for the next Apple and Amazon. It’s unlikely that the next group of winners will look like the last one. It might not even make sense to look for such winners. There might be fewer in the future. It was already very tough to find them in the prior decade.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.