UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

Generally, oil stocks are correlated with the price of oil which makes perfect sense because oil producers sell the commodity. Plus, oil services companies raise prices when oil goes up and are forced to take concessions when they fall. That being said, owning oil stocks can be better than buying the commodity since you the benefit from capital returns. Furthermore, just because these firms produce and service commodities doesn’t mean individual ones don’t have certain competitive advantages. It is optimal to layer on company specific research with macro work. You can potentially make money on multiple fronts.

We are in an interesting position because oil prices have been strong due to the successful vaccination efforts in many leading economies, while oil stocks have been weak. It’s no longer just America that’s getting the job done. As of April 19th, 20.2% of Germans had at least one dose of a vaccine. Brazil seems to be plateauing at a high rate of cases and deaths. Currently 11.7% of the country has gotten 1 dose and 4.3% of the country has been fully vaccinated. We could be a few weeks away from the peak in COVID-19 cases and deaths in Brazil if the vaccines are effective.

While oil prices have been solidly in the low $60s, oil stocks have been cratering. As you can see from the chart above, oil and gas stocks have had the largest negative divergence with the commodity in 15 years. That may be in part due to their extreme rally from early November to early March. Plus, they may have been hurt by the decline in yields. If oil prices stay above $60 or move higher, their stocks could recover. The OIH oil services ETF rose 150% from October 28th to March 10th. Since that top, the index is down 23%. The sector rotation towards reopening value stocks was halted. The 10 year yield fell from 1.75% to 1.56%.

Demand Is Coming Back

This may be a classic case of the market overextending itself and then correcting. Demand for travel and energy will increase later this year. There is about to be a huge amount of pent-up demand for leisure and hospitality this summer. We have seen anecdotal evidence of various employers in the country offering bonuses and higher pay to entry level workers in this industry. We’ve even seen bonuses given out just for good attendance. As you can see from the chart below, month over month flight and hotel searches by US residents were up 46% and 10% in March. In March, Booking.com’s visits were up 16.86% monthly to 261.25 million.

The spike in energy demand is going to end the glut in oil. As you can see from the chart below, oil inventories in June 2021 should be about 270 million barrels above the historical average. The glut should fall to about 50 million barrels by next February. Stocks react quickly, but an actual return to normalcy in the oil market will take a few quarters. The trend is up, but there will be corrections along the way. The uptrend will be driven by long term demand growth from emerging markets combined with the decline in investments in new fossil fuel projects due to low prices and the shift to renewable energy.

The chart below details why we will see a decline in inventories in the next couple months. Global crude demand is projected to be over 100 million barrels per day by the end of June. It’s important to study the historical data. Oil is called a dead industry, yet demand has steadily grown since 2003. The problem for oil prices in the 2010s was excessive supply due to shale. Following that supply shock, we had the COVID-19 virus which was a huge shock to demand. This led to the worst decline in energy stocks in 90 years.

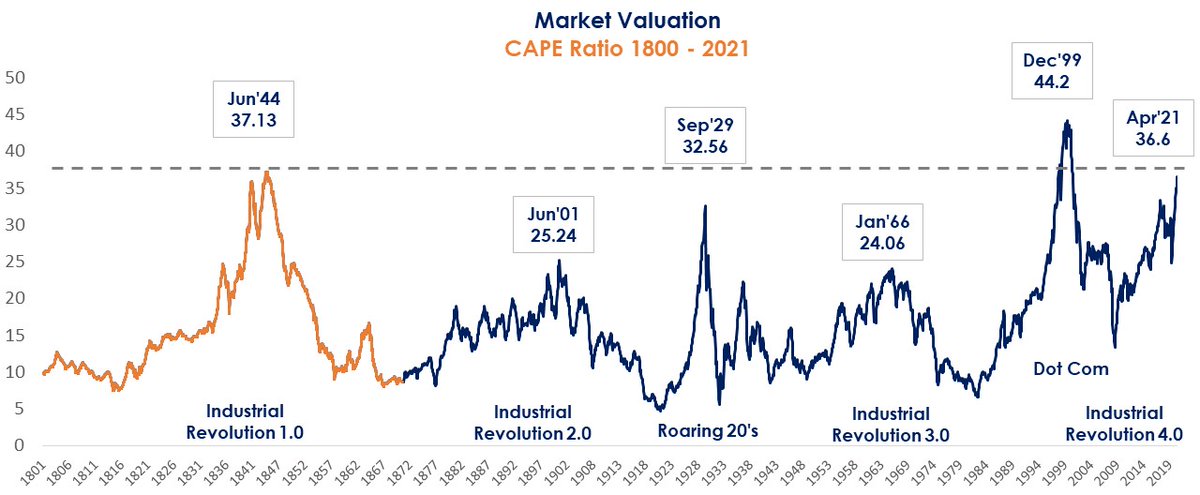

Valuations: Let’s Go Back Further!

The CAPE ratio is very unpopular right now. It’s probably less popular than investing in value stocks or shorting story stocks. It has been shoved away as something that doesn’t work. The CAPE ratio has never been a market timing tool, but since it hasn’t worked for a few years, investors have given up on it. Technically, even after the financial crisis in 2009, the stock market wasn’t extremely cheap. It bottomed slightly below the long term median. However, in the past few decades it has made sense to buy US stocks almost all the time unless valuations are extremely high. Instead of using it as a buy signal, some investors just buy all the time and only use it as a rare sell signal that goes off once every couple of decades.

The current Shiller PE ratio is 37.15 which is well over double the median of 15.82. This is one of those once in a generation moments that the Shiller PE ratio is screaming to sell stocks. They should underperform over the next 10 years. Generally, stocks don’t plateau; they fall sharply. However, low single digits returns in the next 10 years aren’t great either. This chart adds in data from 1800 to 1870 which we are sure is going to anger some readers. Investors don’t think data from before 1980 is relevant. We have never in history had such a long stretch of elevated valuations. Is this the new normal?

Everyone Is Invested

Stocks are near a record percentage of household assets which is exactly in line with how elevated valuations are. One difference in this chart is that the peaks in the late 1960s, late 1990s, and now almost all line up. In the CAPE chart, the bubble in the late 1990s was much more elevated than the one in the late 1960s.

Conclusion

Oil stocks are cratering without oil prices. This might just be a correction from overbought levels. Demand for oil is spiking which is lowering the inventory glut. The US CAPE ratio is exceedingly high. It’s actually within striking distance of the peak in late 1999. Similarly, US households have nearly a record high percentage of their assets in stocks.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.