UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

The March industrial production report wasn’t as amazing as the ISM PMI indicated, but monthly & yearly growth improved sharply partially because of very easy comps. Monthly industrial production growth was 1.4% which increased from -2.6%, but was half of estimates. Yearly growth spiked from -4.8% to 1%. The comp was 4.5% easier, so that’s not as impressive as it seems. Yearly growth was the highest since June 2019 because the economy was in a slowdown in the 2nd half of 2019 and early 2020. The economy was just about to exit its slowdown right when COVID-19 started.

As you can see from the chart below, from February 2020 to March 2021, the industrial production index has fallen from 109.3 to 105.6.

There is still plenty of room for the recovery to go; it’s just that the PMIs have probably peaked or are near their peak. In theory, that means the rate of improvement in industrial production has peaked, but it’s possible the correlation is imperfect. We’re seeing a minor decoupling already in that the March ISM manufacturing PMI was 64.7 (best in decades), yet industrial production growth was just 1.4% (decoupling was greater in February). It’s possible to be more bullish on the actual data than the survey data.

Monthly manufacturing output growth was stronger than industrial production, but it also missed estimates. Growth rose from -3.7% to 2.7% which missed estimates by 0.9%. That’s not that impressive given the very easy comp. That being said, it’s a little closer to its pre-pandemic level than industrial production. The index is down from 106.1 to 104.3. Yearly growth spiked from -4.4% to 3.4%. Just like industrial production, net month’s comp will be the easiest of the cycle. Just like with retail sales, yearly growth will be extremely high. It could even set a record if the regional Fed indexes are a proper early tell for April’s data.

The capacity to utilization rate rose from 73.4% to 74.4%, but we aren’t near overcapacity. Manufacturing was impacted by the semiconductor shortage. Auto manufacturing was up 2.8% monthly. Many auto companies are constrained by the semi shortage. Mining was up 5.7% because of oil. Utilities were down 11.4% because of warm weather. It will be interesting to see how close manufacturing and industrial production get to their pre-pandemic levels in April. If they spike severely, we could be close to the hard data peak especially in rate of change terms.

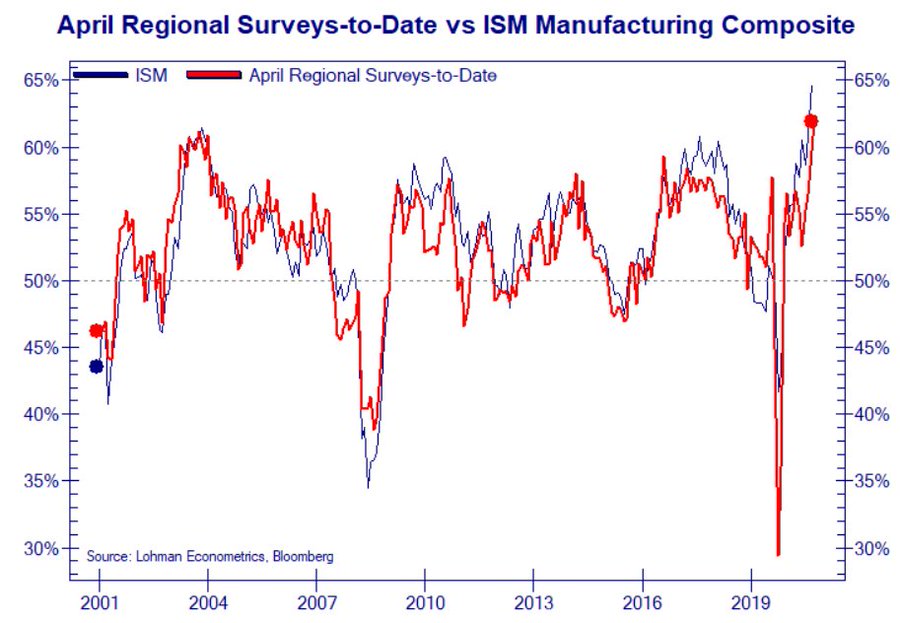

It Doesn’t Get Much Better Than This

We are either at the peak or very close to the peak in regional Fed data. The Empire Fed manufacturing general business conditions index rose from 17.4 to 26.3. That’s the highest reading since October 2017. The new orders index rose 17.8 points which was the highest in at least 5 years. Inflation is roaring. The prices paid and prices received indexes were up 10.3 and 10.7 points to 74.7 and 34.9. As we mentioned, this isn’t reflected in the CPI reading (although April’s CPI will be stronger than March’s).

The Philly Fed index spiked to its highest level in nearly 50 years in April. That explains why the combination of these two Fed indexes is the highest since at least 2001. The chart above shows the manufacturing PMI is projected to be 62 (ISM PMI was above this combo last month). We are undoubtedly near the peak for the cycle.

Specifically, the Philly Fed diffusion index rose from 44.5 to 50.2. Only 8.2% of firms saw a decrease in activity. There is still a lot of inflation. The prices paid and prices received indexes were 69.1 (down 3.5) and 34.5 (up 4.3). Only 2.3% of firms saw a decline in prices paid and just 1.3% had a decrease in prices received. Expectations were extremely optimistic. The index rose from 59.1 to 66.6. 71% of firms expected an improvement in business conditions in 6 months and 4.4% expected them to get worse. It can’t get much better than that.

Could Used Vehicle Inflation Increase Further?

Used car and truck CPI has been high for a while, but it’s about to face much tougher comps in the next few months which makes us think it will fall. Furthermore, you would think as public transportation usage increases once the country is fully vaccinated, demand for used vehicles will fall. However, the Blackrock used vehicle retention index implies used car and truck inflation is about to go vertical as the chart below shows. It will be interesting to see what happens to the Blackrock index this summer after the pandemic is over.

Investor Sentiment

Last week’s AAII investor survey reading showed the highest percentage of bulls since January 2018. Even though stocks didn’t fall, in the week of April 14th, the percentage of bulls fell 3.1% to 53.8% and the percentage of bears rose 4.2% to 24.2%. It’s ideal to see sentiment worsening in a rising stock market, although stocks can’t rise forever either way. The chart below shows a new twist on this index. The 5 year moving average of the bull bear spread is at a new high by far. That’s pretty amazing because last year we had the longest streak ever where there were more bears than bulls. This chart looks a lot like the 10 year Shiller PE ratio. Both imply weak long term forward returns.

Stocks Should Be High

Recently the highest percentage of S&P 500 stocks were above their 200 day moving average ever. However, that might be justified because earnings are so strong. The 1 month breadth of the earnings revision ratio is among the strongest since 1999. Usually that doesn’t last. We aren’t about to see an earnings recession, but revision breadth can’t stay this strong just like how the PMI can’t stay this high.

Conclusion

The March industrial production report was good, but missed estimates. It wasn’t great like the ISM PMI. The regional Fed indexes are the highest of this century. Used car & truck inflation will rise further if it follows the Blackrock index. The percentage of S&P 500 stocks above their 200 day moving averages was the highest ever, but that might be justified due to earnings revisions. Earnings revision breadth will probably fall back down soon along with the PMI.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.