UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

Discussions about a possible earnings recession were prevalent in January and February because earnings estimates collapsed. Uncertainty over the government shutdown, trade war, and hawkish Fed all influenced firms to issue weak guidance. Estimates were cut as analysts use guidance to make their assumptions. Estimates cratered as stocks rallied higher to start the year, possibly because this was all priced in during the bear market in Q4. The debates on this topic have died down because the rate of change in the decline in earnings estimates has moderated. To be clear, according to FactSet the 7.2% decline in bottom up Q1 2019 estimates from the start to the end of the quarter was the largest since Q1 2016 when estimates fell 9.8%. Energy, materials, and technology had the biggest declines as their estimates fell 34%, 16.3%, and 8.3%.

Earnings Revisions Don’t Look Terrible Anymore

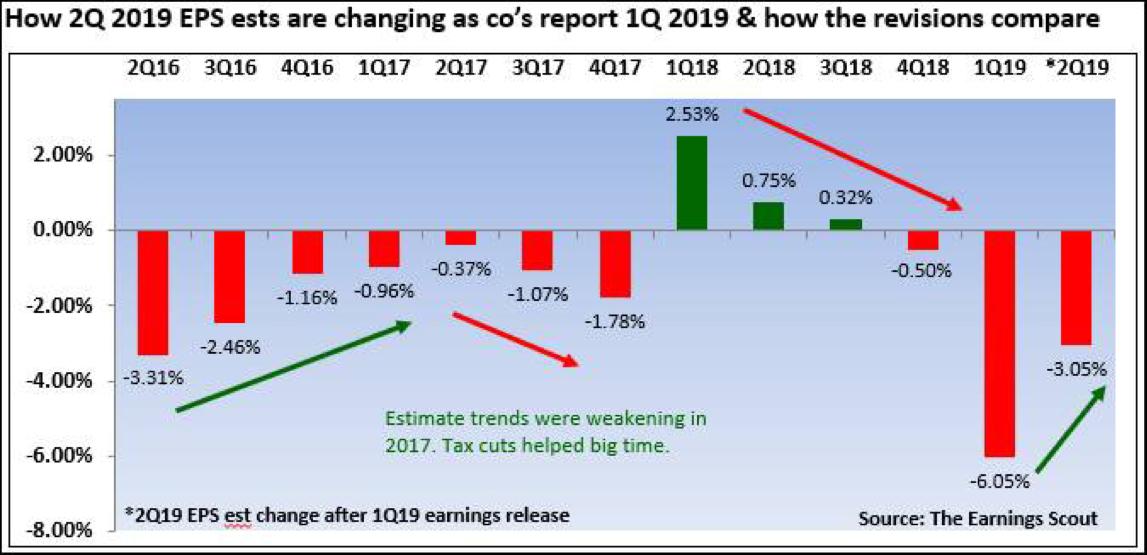

However, as the chart below shows, estimates for Q2 have fallen much less than Q1 estimates after the first 20 firms reported results.

The Earnings Scout believes we must focus on Q2 estimates now that Q1 earnings season is underway. The changes to Q2 estimates tell us about the guidance reported in Q1. So far, the results this quarter haven’t been as bad as feared. 60% of the first 20 S&P 500 firms reporting earnings saw estimates cut. Q2 revisions were -3.05% which is much better than the 6.05% decline at this point last quarter. The results aren’t as good as 2018, but that was a very rare moment catalyzed by the tax cut. Low single digit declines are a good thing.

The latest results include 22 S&P 500 firms. 82% of firms beat EPS estimates on 4.1% growth. However, only 45% of firms beat sales estimates on 5.2% growth. The prior quarter had EPS growth of 26.9% with the first 22 firms reporting earnings. While growth is much lower, the 7.5% average EPS beat is helping firms avoid declines. The dreaded earnings recession looks like it won’t occur. The weakness isn’t as prevalent as bearish investors hyped it up to be. Investors who bought stocks in January and February as estimates fell are sitting in the catbird seat (an enviable position).

92% Chance Of An Earnings Recession

While the first 20 firms have reported solid EPS growth in the face of weak estimates, S&P 500 firms are fighting an uphill battle to avoid an earnings recession. As you can see from the table at the bottom, every single Fed tightening cycle has ended with an earnings recession except in 1994.

In the mid-1990s consumer credit exploded with the highest yearly growth being 15%. The mid-1990s was the start of the housing bubble. That bubble extended the expansion to 10 years. This time American consumers are deleveraging, the Eurozone’s household debt to GDP ratio is falling, and China’s investments to GDP are falling. The same debt driven catalysts that existed on the consumer side in previous decades are less of a factor today to prop up corporate earnings growth.

Even though the ISM manufacturing PMI perked up in March, it’s still roughly following the weakening trend. Bullish investors are hoping the Fed paused its tightening in time, that the manufacturing/global slowdown is near its end, and that the fiscal stimulus pulls through in helping American growth. So far, based on the Earnings Scout’s metrics, we aren’t on pace to see an earnings recession.

Minor Or Deep Earnings Recession?

The size of the earnings recession determines how deep the earnings decline will be. The slowdown in 2015-2016 actually caused an earnings recession worse than some of the ones listed in the table below.

The average earnings decline in mild recessions is only 9%. That leads to an 18% decline in stocks. The average deep recession causes a 25% decline in S&P 500 earnings and a 33% decline in stocks. The earnings recession during the financial crisis took down earnings by 45%. That was by far the biggest decline in earnings since 1948. That makes you question prognostications for a similar event in the next recession especially since consumers have deleveraged. This is something we have discussed at depth previously, here and here. Interestingly, if there’s a mild recession, the average stock market decline is less than the Q4 2018 bear market. The hype around the next recession occurs because people have recency bias; they think the last one is the new normal.

Don’t Invest Yourself?

It’s widely known that most individual investors underperform the market. The bottom chart below goes into detail about how bad it has been. Even though this period includes the housing bust, it includes enough of the run up prior to the decline that homes appreciated almost double the annualized rate the average investor’s portfolio did. The S&P 500 increased 3.7% more per year than investors’ portfolios. That’s a huge difference when gains are compounded.

This shows how difficult it is to beat the market. Being an above average investor still probably means you underperform the market. That’s not to say you can’t invest on your own. You can either invest a portion of your funds on your own, while having a large percentage in an index fund or you can change the stance of your portfolio depending on your macro viewpoint. For example, you can boost your long bond exposure if you see a slowdown coming. Those small shifts avoid huge underperformance risk. (Not advice. Talk to a certified financial adviser)

Discount Sales Drive Redbook

The latest Redbook sales growth from the week of March 30th saw sales increase 4.4% yearly which was down from 5.3% the week before. In the past few months Redbook sales growth has been stronger than other metrics. That’s because Redbook is being pushed higher by discount stores. The green line in the chart below shows discount sales growth and the orange line shows department sales.

The difference between the two as measured by the white bars is the largest since the financial crisis. This means the consumer isn’t doing as well as the headline reading suggests. That being said, it’s also not as bad as the financial crisis or the 2015-2016 slowdown as the Goldman Sachs chain store sales growth is still positive.

Conclusion

The reports from Q1 aren’t as bad as investors calling for an earnings recession projected. Guidance is much better than last quarter. The bad news is usually there is an earnings recession after the Fed tightens. As least the next recession probably won’t lead to another 45% EPS decline because there aren’t consumer bubbles keeping this economy afloat like in previous decades. Unless you are a far better than average investor, it makes sense to keep most of your money in an index fund because the average investor has vastly underperformed every asset class. Their average real returns are -0.3% per year. As the February retail sales report implied, Redbook’s same store sales growth is better than reality. It’s being boosted by discount store sales which isn’t ideal because it means the consumer is under duress.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.