UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 5 minutes

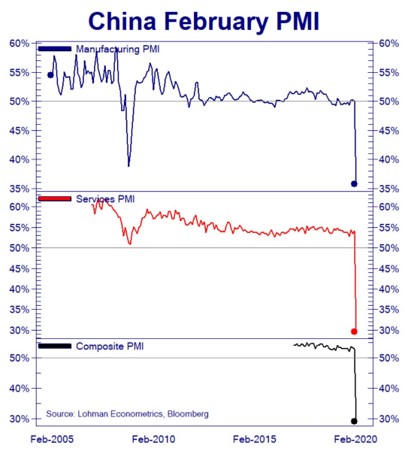

We’ve been consistently making the point that by the time economic data comes in, the market will have long priced in the negative impact of the coronavirus. We saw that on display on Friday as the Chinese February PMI was a disaster, while the Shanghai Composite index bottomed back on February 3rd. The index had been one of the best places to invest in February. It’s still up since its February 3rd bottom, but global selling sent it down 3.71% year to date. The Chinese market impacted the rest of the world a month ago and now the reverse is true (rest of world impacting China).

The scary aspect of this is that the Chinese PMI gives us a glimpse of the potential impact of the coronavirus in other countries. As you can see from the top chart above, the manufacturing PMI fell to 35.7 from 50 which is a record low. Shockingly, the consensus was for a PMI of 46. That’s a bizarre expectation since the economy was shut down for much of the month. That consensus estimate is more surprising than the weak reading. The production index was 27.8, the new order index was 29.3, and the employment index was 31.8.

As the bottom two charts above show, the services and composite PMIs also reached record lows. The services index was down from 54.1 to 29.6. The construction index fell from 59.7 to 26.6. The good news is these are likely the bottoms for these categories as the economy has begun to resume activity. Nomura believes Q1 GDP growth will be 2% and Capital Economics believes it will be negative in year on year terms for the first time since at least the 1990s.

Powell Gives A Small Update

In the midst of this decline in stocks, there have been calls for the Fed to do an intra-meeting cut to surprise the market and promote confidence. The obvious problem is that the Fed can’t come up with a vaccine to save people from this virus. The Fed can’t save the market from panicking over something it doesn’t control. That being said, helping business go on as usual is pivotal to limiting the damage the virus causes. Nothing would be worse than a spike in job losses and a pandemic. In theory, if a business that was trying to create a vaccine didn’t have access to capital, that would be problematic, but the reality is those are the only firms traders have favored in this correction.

In response to the decline in stocks and the worries about the coronavirus, Powell made a rare statement. The fact that he made a statement and didn’t just act to cut rates implies there isn’t an emergency cut coming unless things get worse. Powell stated, “the coronavirus poses evolving risks to economic activity. The Federal Reserve is closely monitoring developments and their implications for the economic outlook. We will use our tools and act as appropriate to support the economy.” This supported the notion that rate cuts are coming which is obvious at this point. The market is pricing in over 3 rate cuts. The least Powell could have done was imply rate cuts are coming. Remember, the Fed’s quiet period starts soon. At its March meeting it will likely cut rates and guide for future cuts. Remember, this is a new cut cycle; it’s not an adjustment like the Fed said last year.

Just because the Fed can’t cure people with the coronavirus doesn’t mean it can’t do anything. As you can see from the chart below, the Oxford Economics financial conditions index spiked to above where it was in December 2018. Remember, that decline in stocks and increase in stress in the financial system was self-imposed. You can see the Fed’s quotes where Powell said the balance sheet unwind was on autopilot and that the Fed funds rate was a long way from neutral. It’s scary how inaccurate that October 3rd comment was. Powell was saying the Fed funds rate was way below neutral, but it seems like the Fed funds rate actually was above neutral as Fed policy tightness helped make the 2019 slowdown worse. If the coronavirus was impacting the economy 6 months ago, we might be in a recession because the economy was weaker then.

This decline in stocks has been liquidity driven. There’s certainly enough liquidity to trade stocks, barring technical difficulties from your broker. Prices moved quickly, but that’s not a problem. The discontinuous action is coming from forced selling. Individual funds don’t have enough liquidity, so they are forced to sell positions to cover for other losses. That’s why you saw stocks like Waste Management fall 8.4% in 2 days. Obviously, we aren’t saying this stock can’t go down. It’s that its business isn’t hurt by the virus.

January PCE Report

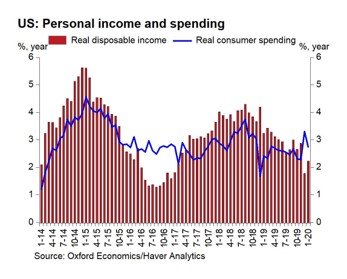

In the midst of the chaos, the January PCE report came out. Before we get to that, recognize the final February consumer sentiment report showed sentiment increased from 99.8 to 101 which is just 0.4 below the cycle high. The U.S. consumer hasn’t been impacted by this virus. Yearly personal consumption expenditures growth fell from 4.9% to 4.5%. The comp got about 0.4% tougher, meaning there was no change in the 2 year growth stack.

As you can see in the chart below, real PCE growth fell from 3.3% to 2.7%. The comp was 0.7% tougher, meaning the 2 year stack ticked up. Disposable personal income growth rose from 3.3% to 4%, but the comp got 1.4% easier. The chart shows real disposable income growth rose from 1.8% to 2.2%. The comp was 1% easier. The decline in consumption growth and the increase in spending growth helped push the savings rate up 0.4% to 7.9% which was the highest level since April.

Headline PCE inflation rose from 1.5% to 1.7% and core PCE inflation rose from 1.5% to 1.6%. Core PCE is below the Fed’s target, so it can cut rates (it will at its March meeting).

Conclusion

It’s no surprise the Chinese economic data is weak. At this point, no one is trading based on the February PMI. The selling is related to the expectation of that weakness coming to other countries. Powell gave us an update because stocks were crashing and financial conditions tightened. He probably won’t discuss cutting rates until the next meeting where there is a 94.9% chance of a cut. The Fed’s quiet window is coming, so it can’t help markets with rhetoric if they keep crashing. The January PCE report was fine. The U.S. economy was doing well up until the coronavirus hit.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.