UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

With the 30 year US treasury yield near its record low which was reached in July 2016, this recent rally is nearly historic. The 30 year yield is closest to a new low (compared to other maturity dates) because the yield curve is flatter than it was during the treasury rally in 2016. Many parts of the curve have already inverted. The later maturity part of the curve is debatably the most important now because the inversion in the near term part of the curve can be explained by saying the Fed is simply behind the market when it comes to rate cuts. The Fed being behind the curve temporarily might not mean a recession is coming. However, the relatively low 30 year yield strengthens the yield curve’s call for a slowdown/recession. The next monthly NY Fed model update, which looks at the yield curve, will show higher odds of a recession in the next year than the prior update.

It’s a simple explanation as to why the 30 year yield has fallen. Growth and inflation expectations have fallen. That’s in tune with the recession call as the deeper the slowdown, the more likely it will turn into a recession. The catalyst for a recession doesn’t need to be large if the economy isn’t growing robustly.

Fund Managers Love Bonds

As you can see from the August Bank of America survey, a net 43% of fund managers expect lower short term rates and 9% expect higher long term rates in the next year. That’s the most bond bullish survey since November 2008.

It’s surprising the 30 year bond yield hasn’t hit its record low given the relative bullishness as compared to 2016. This survey is showing similar readings to 2007 right before the financial crisis. A massive recession which poses a risk to the financial system may not be likely, as we discussed in this article, but economic weakness is being priced in.

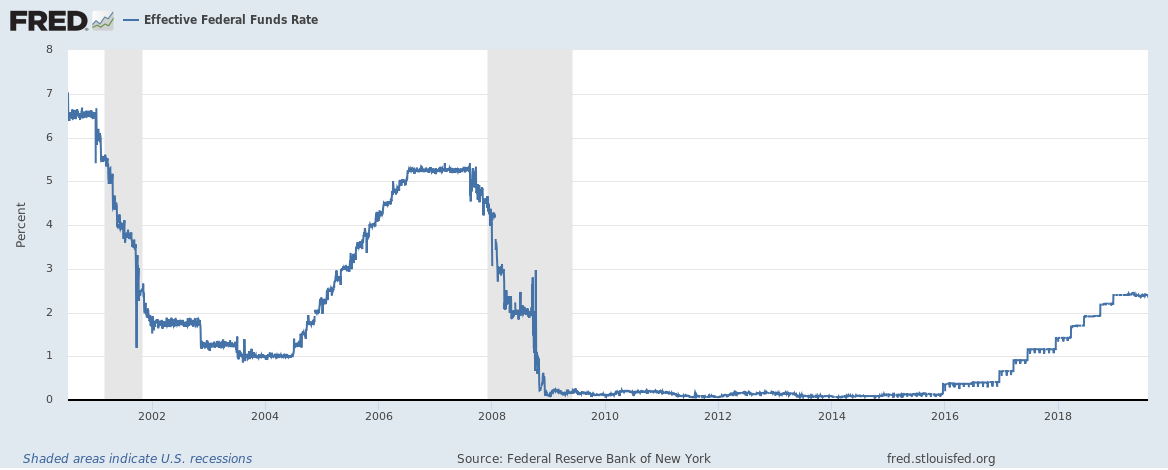

How Low Can Rates Go?

Negative interest rates draw a lot of attention because they are a new phenomenon. Even if you have no interest in investing, you are curious about how this all works. JP Morgan did analysis in 2016 which shows how low policy rates can go without putting impossible pressure on bank profits or creating a major incentive to move to cash.

Essentially, this tells us the lowest central banks can cut rates without near term major negative impacts. It was previously assumed that rates wouldn’t go below zero, but recent policy decisions around the world have proven otherwise.

Specifically, JP Morgan found that based on the Swiss central bank’s policy, Euro rates can get to -4.5%. The bounds in the US and the U.K. might be -1.3% and -2.5%, but they might be able to go lower. With core PCE inflation never sustaining above 2% this cycle, the Fed probably didn’t need to raise rates as high as it did if you work based on the assumption that it can cut rates below zero. In this case, the Fed has more capacity to cut rates to combat the next recession than previously thought.

Corporate Debt A Problem?

The decline in interest rates is partially why corporate debt has increased significantly in this expansion. This explains why the chart below shows a record net percentage of fund managers saying firms are overleveraged.

To be clear, just because a much higher percentage of managers are concerned about corporate leverage than in 2008 and 2009 doesn’t mean the issue is worse. It just means the consensus of it being at least somewhat an issue is more universal.

Interestingly, in Q1 2009, non-financial corporate debt as a percentage of the market value of corporate equities was 69%; it’s 34% in Q1 2019. The percentage spikes when equities fall; based on last cycle, it’s odd to see the current concern rising before the fall in equities. On the other hand, corporate debt to GDP is near a record high. However, corporations are more internationally focused, so domestic GDP isn’t the perfect divisor. Corporate debt will only be an issue outside of a recession if rates rise. As we saw previously, managers don’t see rates rising. Junk debt is always an issue during recessions because profits dwindle, and financial conditions tighten (spreads widen). It’s an open ended question if it will become more of an issue in this cycle.

Managers Still Bearish

Fund mangers are still concerned about equities if not outright bearish. As you can see in the chart below, 33% of fund mangers have taken out protection against a big decline in stocks in the next 3 months.

51% haven’t taken out protection. That’s the highest net percentage in the history of this survey which was started in 2008. There’s not much more concern that can be in the market than there is now. That’s only a bullish sign if you don’t see a recession coming. These managers might be correct.

Value Stocks Loved Again

The chart below shows a net -5% of fund managers expect value stocks to outperform growth stocks in the coming year. (Ignore side caption; it’s wrong).

You’d think value might be less likely to face risk than the high multiple growth stocks on an equal weight basis. However, the value factor is overweight energy and financials which isn’t a great place to be with the expected global decline in oil demand growth due to the slowdown and the inversion and decline in yields which is hurting the banks.

Conclusion

This is a new period where there has been an increase in negative interest rates. The US 30 year treasury yield is near its record low, showing us the possibility of yields getting closer to zero in the US. According to JP Morgan, the Fed can cut rates below zero without immediate terrible ramifications. Fund managers are bullish on treasuries and nervous about a decline in equities in the coming months. They are also worried about corporate leverage. Finally, they don’t see value stocks outperforming growth stocks probably because they aren’t bullish on the energy and financial sectors.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.