UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

The February BLS report is expected to show 175,000 overall jobs created and 183,000 private sector jobs added. The ADP report came in much below that, disappointing economists. It’s anyone’s guess if this means the BLS report will disappoint. We think the jobs report will be decent because there are early signs the economy is starting to recover following the 3rd wave of COVID-19.

ADP showed private sector job creation of only 117,000 jobs which was below estimates for 165,000. That’s 66,000 below the estimate for private sector job creation in the BLS report. Within the report, small business job creation was the weakest at only 17,000. We think small business job creation will be very strong this summer as restaurants reopen. There will be a huge turnaround. In late 2020 and early 2021, people were raising money to keep restaurants open. This summer, you won’t be able to get a table at many popular restaurants because they will be so busy. They will be hiring like crazy very soon.

Mid-sized firms added 64,000 jobs and large firms added 44,000 jobs. The goods producing sector lost 13,000 jobs. Natural resources and mining actually lost 4,000 jobs. It’s possible that’s related to the poor winter weather in Texas. It’s tough to see this continuing because the oil & gas industry is starting a cyclical upturn.

The service providing industry added 138,000 jobs. Leisure and hospitality only added 19,000 jobs which isn’t much compared to what is to come. Texas and Mississippi just ended their mask mandates and health restrictions because of the decline in national hospitalizations. This should lead to growth in the leisure and hospitality industry starting as early as March. Education and health added 41,000 jobs which was the most out of any group. It’s great to see healthcare jobs coming back because it means people are getting elective surgeries again. Just because a surgery is elective doesn’t mean it’s not incredibly necessary.

Very Strong IHS Markit PMI

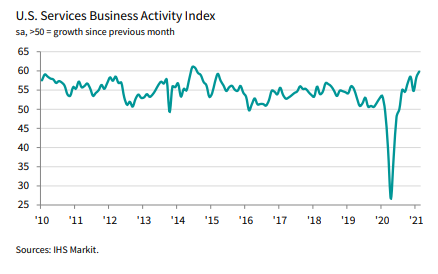

The business cycle is starting to get ramped up. The IHS Markit services PMI was the highest since July 2014 which pushed the composite PMI to the highest reading since August 2014. Cost pressures were the strongest on record going back to October 2009. The problem with getting CPI to go up is it is driven by shelter costs which aren’t part of the costs in this Markit calculation. Shelter inflation is being suppressed by the eviction moratorium and the weakness in cities. In the services segment, job creation was barely positive. Growth was the lowest in the 8 month expansion. Optimism on expectations was slightly below January which is weird because the vaccination rollout has gone well.

The service PMI rose from 58.3 to 59.8 which was even above the flash figure of 58.9. That means the service sector got even better in the 2nd half of the month. That makes sense because the vaccination rate improved throughout the month. We think America’s quick vaccination distribution compared to most developed nations explains why its PMI is doing so much better than other countries. As you can see from the table below, the services PMIs of the U.K., France, Japan, Germany, and Italy were all below 50 which indicates a contraction. India’s PMI was the 2nd highest on this list at 55.3. This is because the country might have reached herd immunity. Since September, cases per day in India have fallen from over 90,000 to about 16,000.

Expected Boom In Global Personal Consumption

There is going to be a boom in consumption in the middle of the year led by America which is one of the closest countries to getting control of the virus. As you can see from the chart below, JP Morgan believes Q1 global consumption growth will be 1.9%.

The middle quarters are expected to see 8.5% growth. This brings JP Morgan’s global GDP growth estimate to 7.6%. This will be the much vaunted global synchronized acceleration. Generally, when this type of synchronization occurs, it’s time to get defensive because they don’t last long. However, it hasn’t even happened yet; it’s too early to get defensive. That’s a strategy for 6 months from now.

Quant Indicator Is Almost Bearish

The chart below shows a quant indicator that’s based on sell side recommendations. It gives off a bearish warning when the sell side gets too positive. The sell side hasn’t given off a bearish warning since 2007 which was right before the financial crisis. The sell side, of course, was extremely euphoric leading up to and after the tech bubble which was a major sell signal. Just about every indicator was screaming caution in the late 1990s, but momentum investors didn’t care.

The Promised Land

2021 has been a great year for value investors. The much talked about shift from growth to value is finally here. As you can see from the chart below, growth is finally losing to non-growth after a massive run for growth in the prior few years. Growth beat non-growth by 42% in 2020. It beat non-growth in 11 of the past 13 years.

Value stocks usually do well in the beginning of recoveries because they are mostly cyclicals. That’s the place to be in this economy. The reopening and $1.9 trillion stimulus will make this look like the early cycle economy that it is. Economic growth is expected to catch up to the pre-recession trend unlike after the last recession. GDP growth never recovered its financial crisis losses.

Conclusion

The ADP report was weak. We don’t know if that means the BLS report will be weak. The ADP report has had a bad track record since the recession. The IHS Markit PMI was extremely strong. It hit a 6.5 year high. The US services PMI is much stronger than the rest of the world. Global consumption growth will rocket higher in Q2 and Q3. The sell side is close to giving off a euphoric (bearish contrarian) warning signal. Non-growth is finally beating growth this year which has been a rarity in the past 13 years.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.