UPFINA's Mission: The pursuit of truth in finance and economics to form an unbiased view of current events in order to understand human action, its causes and effects. Read about us and our mission here.

Reading Time: 4 minutes

We got the hotly anticipated March CPI report on Wednesday. It wasn’t anything to write home about. This was only expected to be the start of higher inflation. The peak won’t be until this summer after the US hits heard immunity. Specifically, month over month headline CPI was 0.6% which rose 2 tenths from the prior month and beat estimates by 1 tenth. The 10 year yield is currently at 1.55% which is about 22 basis points off its high this year. The bond market wasn’t impressed by this slight beat. Furthermore, core monthly CPI was 0.3% which was up 2 tenths from February and beat estimates by 1 tenth.

On a yearly basis, base effects played a strong role in the increase. Headline CPI rose from 1.7% to 2.6% which beat estimates by 1 tenth. Core CPI was up from 1.3% to 1.6% which met estimates. Core CPI is still below the Fed’s target. That’s remarkable given the extremely high readings in the prices indexes in the ISM and Markit monthly PMIs. If you listen to public companies, they sound nothing like the core CPI reading. Everyone is talking about higher costs. 1.6% core inflation is miles away from what we are seeing in the real world.

As you can see from the chart below, energy drove overall inflation higher. Energy inflation was 13.2%. Energy commodities had a massive 22% increase. It will be interesting to see next month’s reading. Remember, in April 2020 oil prices went negative temporarily.

Food inflation was 3.5%. Food away from home inflation was 3.7%. This was driven by limited service meals and snacks which had 6.5% inflation. Full service meals and snacks only had 3.2% inflation. That will spike in April because people are starting to have normal in-person meals. On April 19th in NYC the curfew for dining will extend 1 hour to midnight. The curfew will be 1 AM for catering. There won’t be any curfews by May if the vaccination process goes well.

Core Inflation Was Low Due To Rent

Now let’s look at the low core inflation rate. Core commodities inflation was 1.7% and core services inflation was 1.6%. There was nothing new in the commodities category. Used car and truck inflation was 9.4%. The comps are about to get very tough which should lower yearly growth. However, there is still a shortage of used vehicles. Public transit usage hasn’t gone back to normal. We have yet to see a spike in supply due to people selling their vehicles because their habits are going back to normal. Maybe people won’t use public transport as much as they did before the pandemic. That’s terrible for the environment. Public transportation is much greener than electric vehicles.

Within the services category, medical care services inflation was 2.7%. We are about to see a spike in elective procedures now that the risk of catching the virus has diminished substantially. The 7 day moving average of deaths in America has fallen to 747. On the negative side, the latest wave in Michigan hasn’t abated yet. Look for that to abate within the next few weeks as more people get vaccinated. Shelter inflation was just 1.7%. Core inflation will never get to above 2% without shelter inflation getting above 2%.

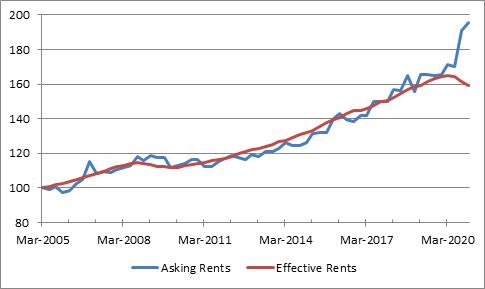

The chart above isn’t from the CPI report, but it shows a key point about rents. If a landlord is unsure of whether they’re able to collect rent, it goes to zero. This uncertainty increases with eviction bans in place. As you can see, asking rents have exploded, but effective rents have fallen. Look for the trend in effective rents to reverse within the next few months. Rent inflation is going to drive shelter inflation higher by the end of the summer.

There is no reason people won’t be able to pay their rent once all the leisure and hospitality jobs come back. There should be even more job creation in April. The current federal eviction moratorium ends on June 30th. It’s hard to see that being extended much longer with the pandemic near its close. 30.5% of Americans have been vaccinated. We are 3 months from 75% of the country being vaccinated (assuming that many want to be vaccinated).

Cash Out Refinances Spike

It sounds extremely weird to hear that shelter inflation is low because housing is on fire. This is the strongest housing market since the peak of the past bubble. CPI uses owners’ equivalent rent which is different from the Case Shiller index. In fact, Moody’s is predicting 9.9% price growth in 2021. Zillow sees 10.3% growth. It is a bonanza. Stories of bids well above the ask are very common. If you expect to pay the ask price, you are in for a rude awakening. There is a massive shortage in entry level housing in America.

It’s no surprise with the massive spike in housing prices that we are seeing a large increase in net equity cashed out in refinancing of prime conventional loans. As you can see below, at $48 billion, we are a little above half the peak in 2006. This level probably has a little room to get even higher. Remember, this isn’t a true bubble in housing because demand is coming from well-qualified buyers. On the other hand, in hindsight economists will call this a bubble if rates spike. We’d need to see the 10 year yield to spike to 3% to make a difference. There won’t be a bust like in 2008, but prices would fall if rates spiked.

Conclusion

The CPI report was nothing to get excited about. That’s because low rent inflation suppressed core inflation. In the real world, prices are screaming higher. The US housing market is on fire. This is due to demographics and low interest rates. If rates spike, prices will fall. However, there won’t be another bust because buyers are well qualified. If anything, the housing market is getting healthier as people get their jobs back. The forbearance rate has been steadily falling in the past year.

Have comments? Join the conversation on Twitter.

Disclaimer: The content on this site is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Please read full disclaimer and privacy policy before reading any of our content.